Serving Chicago & all 50 states Mon-Fri 9am-6pm CT

Qualified Small Business Stock (QSBS) in 2025: How to Make Up to $10M+ of Your Exit Completely Tax-Free

Unlock the power of QSBS in 2025: Exclude up to $10 million (or more) in capital gains tax-free on your startup exit. Full guide to eligibility, 83(b) elections, pitfalls, and planning strategies for founders and investors.

Tram Le, CPA

1/5/20264 min read

Picture this scenario: It's 2025, and after seven grueling years of building your startup from a garage idea into a thriving company, you finally get an acquisition offer. The deal values your shares at $15 million—a life-changing exit. Under normal capital gains rules, you'd owe roughly $3.57 million in federal taxes alone (at the 23.8% top rate including NIIT). But because you structured properly from day one, you qualify for Qualified Small Business Stock (QSBS) treatment under Section 1202—and pay $0 federal tax on up to $10 million (or more) of that gain.

This isn't hype. The QSBS exclusion is one of the most powerful tax incentives in the Internal Revenue Code, and thanks to the One Big Beautiful Bill Act (OBBBA) making the 100% exclusion rate permanent beyond 2025, it's more valuable than ever for founders, early employees, and angel investors.

Yet many startups miss out entirely—either by choosing the wrong entity, missing key elections, or triggering disqualifying events. Let's break down everything you need to know to capture this massive benefit.

What Exactly Is QSBS and Why Does It Matter?

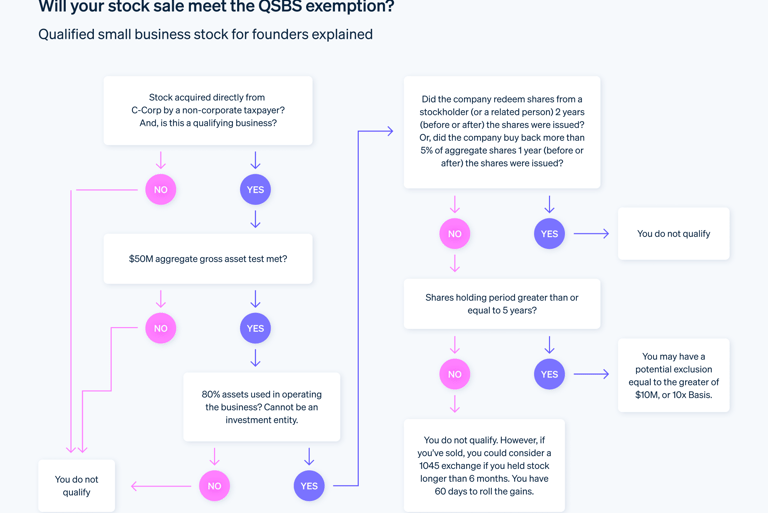

Section 1202 allows eligible taxpayers to exclude up to 100% of capital gains from the sale of qualified small business stock held for more than five years. The exclusion applies to:

100% of gains for stock acquired after September 27, 2010

The greater of $10 million lifetime per taxpayer per issuing company or 10 times your adjusted basis

No Alternative Minimum Tax (AMT) and no 3.8% Net Investment Income Tax (NIIT) apply to the excluded amount. For high-net-worth founders or early employees, this can save millions.

Real-world impact: A founder who invests $200,000 early and exits with $12 million in gain can exclude the full $10 million limit—saving ~$2.38 million in federal taxes. The remaining $2 million is taxed normally, but that's still an enormous win.

Strict Eligibility Requirements: The Five Key Tests

QSBS rules are unforgiving—one misstep can disqualify everything. Here are the core requirements:

Must Be a Domestic C-Corporation The issuing company must be a U.S. C-corp at the time stock is issued and when sold. LLCs, S-corps, and partnerships don't qualify. This is why nearly every venture-backed startup incorporates (or converts) to C-corp early.

Gross Assets Test: ≤ $50 Million The company's gross assets (cash + adjusted basis of property) must not exceed $50 million:

At the time of stock issuance

Immediately after issuance (including proceeds from the stock sale itself)

Track this carefully during funding rounds—large cash raises can push you over if not monitored.

Active Business Requirement At least 80% (by asset value) of the corporation's assets must be used in an active qualified trade or business. Disqualified businesses include:

Professional services (law, accounting, consulting, health, financial services) where reputation or skill of employees is the principal asset

Banking, insurance, financing, leasing

Farming, mining, hospitality (hotels/restaurants)

Investment companies or holding companies

Tech, software, manufacturing, biotech, and most product-based startups generally qualify.

Original Issuance Requirement You must acquire the stock directly from the company at original issuance in exchange for money, property (not stock), or services. Secondary purchases (from other shareholders) don't qualify unless through specific exceptions.

Five-Year Holding Period Stock must be held more than five years from issuance date to sale/exchange. Gifts and inheritances can carry over holding periods.

Critical Planning Strategies Every Founder Should Know

QSBS success starts at formation—here's how to maximize it:

File an 83(b) Election for Restricted Stock Most startup stock is restricted and vests over time. Without an 83(b) election (filed within 30 days of grant), you pay ordinary income tax as shares vest—and the holding period starts later. With 83(b):

Pay tax upfront on fair market value (often near $0 early)

Convert all future appreciation to capital gains

Start the 5-year QSBS clock immediately

Miss the 30-day window? No do-over.

Leverage Section 1045 Rollover If you sell QSBS before five years or want to defer gain, reinvest proceeds into new QSBS within 60 days. This defers recognition and can preserve/restart eligibility.

Avoid Disqualifying Redemptions Significant stock buybacks from you (or related parties) around issuance can taint the stock. Plan repurchases carefully.

Document Everything Maintain records proving:

Asset test compliance

Active business use

Original issuance

Holding periods

Common QSBS Pitfalls That Kill Eligibility

Starting as LLC then converting too late (pre-conversion interests may not qualify)

Performing disqualified services (e.g., consulting-heavy early revenue)

Large redemptions or stock recyclings

Failing to file 83(b)

Raising in structures that push assets over $50M prematurely

State Tax Conformity: Not All Good News

While federal exclusion is 100%, states vary:

Full conformity: Most states (NY, TX, etc.)

Partial/no conformity: California (taxes gains normally), others limit exclusion

Plan for state taxes even if federal is zero.

QSBS Eligibility Quick Checklist

Incorporated as domestic C-corp? □

Gross assets ≤ $50M at/all after issuance? □

≥80% active qualified business? □

Stock acquired at original issuance? □

83(b) election filed (if restricted)? □

Held/will hold >5 years? □

If you check all boxes, you're positioned for massive tax savings.

Real-World Examples

Early Founder: Invests $50,000 in 2019. Company sells 2025 for valuation giving founder $18M gain. Excludes $10M → saves ~$2.38M federal.

Early Employee: Granted options at $0.10/share FMV. Exercises early, files 83(b). Vests over 4 years, holds 1+ more. Exit gain fully excludable up to limit.

Angel Investor: Buys shares in Seed round. Holds through Series C exit. Excludes gains up to their personal $10M limit.

Final Thoughts: QSBS Is "Set It and Forget It" Planning

The beauty of QSBS is that proper setup early requires minimal ongoing effort—yet delivers enormous payoff on exit. But the rules are strict and irreversible in many cases.

If you're a founder, early employee, or investor in a C-corp startup, review your QSBS status now. One small oversight can cost millions.

Ready to confirm your eligibility or optimize your structure? Schedule a complimentary QSBS review with our team—we specialize in helping startups capture every dollar they're entitled to.

This article is for informational purposes only and does not constitute tax advice. Tax laws are complex and individual circumstances vary. Always consult a qualified CPA or tax attorney for personalized guidance.

Get in touch

Contacts

312-544-9226

tram.le@letaxfirm.com