Closing a Business: The 2026 IRS Compliance Master Checklist

Closing a business in 2026? Follow this IRS compliance checklist to end payroll taxes, file your final return, and avoid personal liability. Secure your clean exit.

Tram Le, CPA

3/13/20264 min read

Introduction: Why a "Quiet Exit" is a Risky Strategy

In the world of tax compliance, there is no such thing as a business that simply "stops." Whether you are retiring, dissolving a partnership, or closing a corporation, the IRS expects a formal conclusion. If you fail to "tell" the IRS you are closed, they will continue to expect returns, eventually triggering automated non-filer notices, penalties, and even "zombie" audits years after your doors have shut.

Closing a business in 2026 requires more than just canceling your lease. It requires a systematic deactivation of your tax footprint. This guide provides the authoritative roadmap to ensuring you walk away without a trailing tax liability.

1. The Income Tax Return: Checking the "Final" Box

The most important step in signaling your closure to the IRS is your final income tax return.

For Sole Proprietors (Schedule C): There is no "final" checkbox on Schedule C itself. Instead, you simply report your income and expenses for the partial year and ensure the business doesn't appear on your return the following year.

For Partnerships (Form 1065) and S-Corps (Form 1120-S): You must check the box "Final Return" on the first page of the return.

Final K-1s: You must also check the "Final K-1" box for every partner or shareholder. This allows them to calculate their final "basis" and determine if they have a deductible loss on their investment in the business.

2. Corporate Dissolution: Form 966

If your business is a C-Corporation or an S-Corporation, you have a unique requirement: Form 966, Corporate Dissolution or Liquidation.

The 30-Day Rule: You are legally required to file Form 966 within 30 days of the plan to dissolve or liquidate.

The Attachment: You must attach a certified copy of the resolution or plan to dissolve (your corporate minutes) to the form.

Why it matters: This form is the "official" notice to the IRS that the legal entity is being dismantled, preventing them from looking for future corporate tax filings.

3. Payroll Taxes: The "Trust Fund" Danger Zone

This is the area where most business owners face personal financial ruin. If a business fails, the IRS can hold the owners personally liable for unpaid payroll taxes (specifically the employee’s share of Social Security and Medicare), even if the business was an LLC or Corporation.

Your Final Payroll Steps:

Final Form 941: Check the box on Line 17 (or the 2026 equivalent) stating you have closed or stopped paying wages and enter the final date wages were paid.

Final Form 940: File your final Federal Unemployment (FUTA) return and check the "Final" box.

W-2s and W-3s: You must issue W-2s to your employees by the standard January deadline of the following year, but it is best practice to issue them immediately upon closure.

The 2026 1099 Rule: Remember that for 2026, the threshold for filing 1099-NEC for contractors has increased to $2,000. If you paid a contractor more than $2,000 during your final year, you must issue a 1099 and file the "Final" Form 1096.

4. Disposing of Business Assets: Form 4797

When you close, you likely sold or "distributed" assets like computers, vehicles, or machinery.

The Sale: If you sold equipment for more than its "adjusted basis" (Cost - Depreciation), you have a gain.

The Distribution: Even if you just took the company laptop home for personal use, the IRS treats that as a "sale" at Fair Market Value to yourself.

Reporting: Use Form 4797, Sales of Business Property, to report these gains or losses. This form coordinates with your final return to determine how much of that gain is "Depreciation Recapture" (taxed at higher ordinary rates).

5. Deactivating the EIN: The Final Letter

The IRS never truly "cancels" an Employer Identification Number (EIN) because it is a permanent record. However, you can close your business account associated with that EIN.

The Letter: You must send a physical letter to the IRS (typically to the Ogden, UT or Cincinnati, OH service centers).

Include: The legal name of the entity, the EIN, the business address, and the reason for closing (e.g., "Business dissolved on 06/30/2026").

Requirement: The IRS will not close the account until all final returns have been processed and all balances are paid to zero.

6. Record Retention: The 7-Year Rule

Just because the business is gone doesn't mean the records can be. In 2026, the IRS has increased its focus on "look-back" audits.

Keep for 3 Years: General income tax records and supporting receipts.

Keep for 4 Years: All employment tax records (941s, 940s, and proof of deposits).

Keep for 7 Years: Records relating to property, bad debt deductions, or if you filed a claim for a loss from worthless securities.

Digital copies: Cloud-based storage is acceptable, but ensure you have a "successor in interest" who has the login credentials.

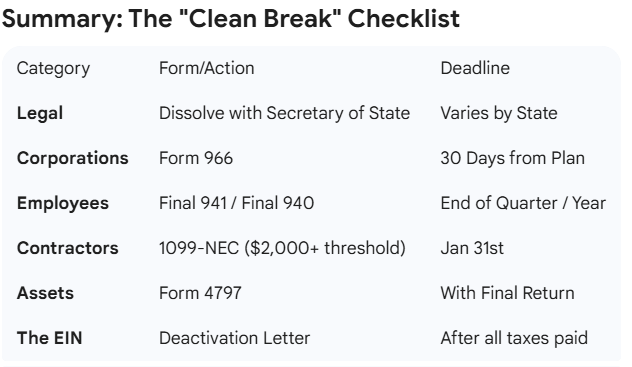

Summary: The "Clean Break" Checklist

Conclusion: Exit with Confidence

Closing a business is an emotional and logistical challenge. By following this compliance roadmap, you ensure that the legacy of your business isn't a mountain of IRS debt and legal notices. When you check that "Final Return" box, make sure your books are reconciled, your assets are reported, and your payroll is settled.

Get in touch

Contacts

312-544-9226

tram.le@letaxfirm.com