Serving Chicago & all 50 states Mon-Fri 9am-6pm CT

Choosing the Right Entity for Your Startup in 2025: LLC vs. C-Corp vs. S-Corp – Don't Lose Millions on Exit

LLC, C-Corp, or S-Corp in 2025? Compare taxes, fundraising, QSBS eligibility, and compliance to pick the best structure for your startup's growth, funding, and exit goals.

Tram Le, CPA

1/16/20263 min read

One of the first questions every founder asks is, “What entity should I form?” It feels like a simple administrative step—pick something on LegalZoom and move on. But this choice quietly shapes your taxes, fundraising ability, equity grants, and ultimate exit for years to come.

I’ve seen founders lose millions in tax benefits because they started as an LLC and didn’t convert in time. I’ve also seen bootstrapped businesses overcomplicate things with a C-corp when they never planned to raise venture capital. In 2025, with permanent Qualified Small Business Stock (QSBS) rules and investor preferences unchanged, getting this right early is more important than ever.

Let’s walk through the three main options—LLC, C-Corp, and S-Corp—in plain language, with real-world scenarios to help you decide.

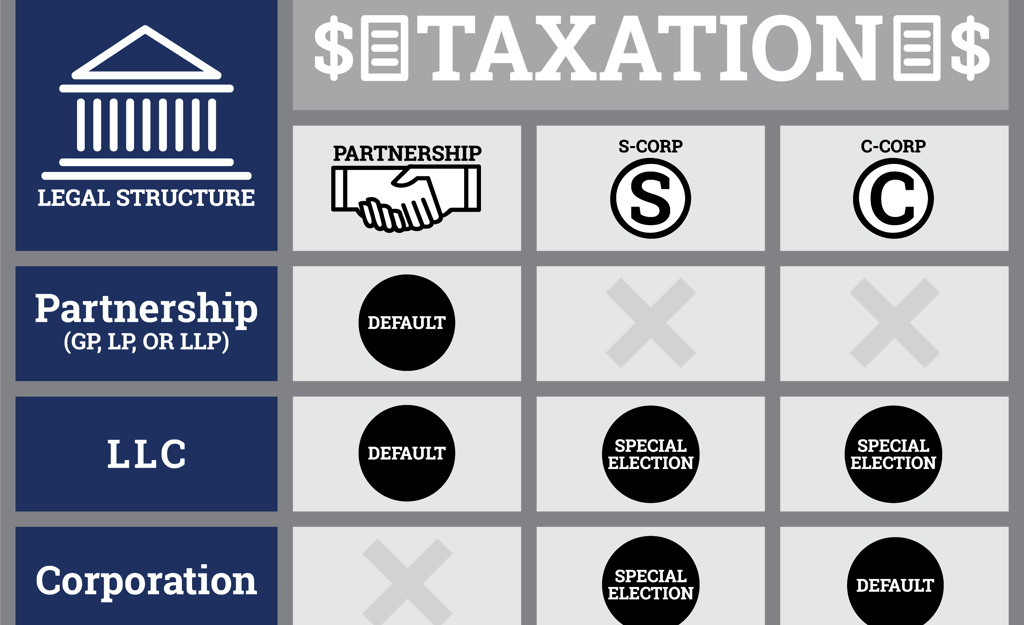

The Flexible Favorite: Limited Liability Company (LLC)

Most founders default to an LLC because it’s simple and flexible.

How it works: By default, a single-member LLC is ignored for tax purposes (you report everything on your personal Schedule C). Multi-member LLCs are taxed as partnerships. Income, losses, and deductions “pass through” to your personal return—no corporate-level tax.

Key advantages:

Easy setup and low ongoing compliance (no board meetings, fewer filings)

Flexible profit allocations (you can split profits unevenly among members)

Losses can offset other personal income (subject to basis and at-risk rules)

No double taxation on distributions

Downsides that bite startups:

Venture capitalists and most institutional investors almost never invest in LLCs (hard to issue preferred stock, complex K-1s)

No eligibility for QSBS tax-free gains

All net income subject to self-employment tax (15.3%) unless you have an S-corp election overlay (rare)

Best for: Bootstrapped businesses, lifestyle companies, consulting firms, or real estate holdings that don’t plan to raise VC or have a big liquidity event.

The Venture-Backed Standard: C-Corporation

Nearly every company you admire that raised serious funding—think Airbnb, Stripe, or your favorite YC startup—is a Delaware C-corp.

How it works: The corporation pays tax on its profits (21% federal rate in 2025). When you distribute dividends or sell shares, shareholders pay tax again—hence “double taxation.”

Key advantages:

Eligible for QSBS: Exclude up to $10 million (or more) in gains tax-free after five years

Investors love it: Easy to issue preferred stock, multiple classes, stock options (ISOs), and convertible notes

Unlimited shareholders of any type (corporations, foreigners, etc.)

Can retain earnings in the company for growth without immediate personal tax

Deduct fringe benefits more easily

Downsides:

Double taxation on dividends (though most startups never pay dividends)

More compliance (board requirements, annual reports)

Best for: Any startup that might raise angel, seed, or VC money, or that dreams of a big exit. If QSBS is on your radar, this is non-negotiable.

The Middle Ground: S-Corporation

An S-corp is essentially a C-corp that elects pass-through taxation.

How it works: Profits and losses flow through to shareholders’ personal returns, avoiding corporate tax.

Key advantages:

Avoid self-employment tax on distributions (only salary is subject to payroll taxes—reasonable salary required)

Single layer of tax like an LLC

Losses can offset other income

Major limitations:

No QSBS eligibility

Maximum 100 shareholders, all must be U.S. citizens/residents

Only one class of stock (no preferred shares—VC dealbreaker)

No corporate or trust shareholders (except certain trusts)

Best for: Profitable small businesses with a few owners who want to minimize payroll taxes but don’t need VC or QSBS.

Real-World Scenarios to Guide Your Choice

Scenario 1: You’re bootstrapping a SaaS tool with your co-founder, expecting steady profits but no outside funding. → Start with an LLC (or consider S-corp later for payroll tax savings).

Scenario 2: You’re building an app, talking to angel investors, and dreaming of a $50M+ exit. → Incorporate as a Delaware C-corp from day one.

Scenario 3: You run a profitable marketing agency with five employees and no plans to sell or raise money. → S-corp can save thousands annually on self-employment taxes.

Scenario 4: You started as an LLC but just closed a seed round. → Convert to C-corp ASAP (usually tax-free if done correctly), but know pre-conversion membership interests may not qualify for QSBS.

The Conversion Question

Many founders begin as LLCs for simplicity, then convert to C-corp before serious fundraising. This can be tax-free under Section 351 if structured properly, but timing matters for QSBS—only stock issued after conversion gets the full benefit.

Quick Decision Flowchart

Ask yourself:

Do you plan to raise institutional money (angels, VCs)? → Yes → C-Corp

Do you want QSBS tax-free exit potential? → Yes → C-Corp

Are you profitable and want to minimize payroll taxes? → Consider S-Corp

None of the above? → LLC is fine

Final Advice

There’s no universal “best” entity—it depends on your goals. But the cost of getting it wrong grows exponentially. Changing later can trigger taxes, complicate cap tables, or permanently disqualify QSBS.

Talk to a startup-savvy CPA early (ideally before you file your first tax return). A one-hour consultation now can save millions later.

Not sure where you stand? We offer complimentary entity reviews for founders—let’s make sure your structure matches your vision.

This article is for informational purposes only and does not constitute tax advice. Always consult a qualified professional.

Get in touch

Contacts

312-544-9226

tram.le@letaxfirm.com